Key Findings

- End-to-end system readiness for developing-nation SmallSat programs sits at TRL 3-5, gated by mission operations and data exploitation, despite satellite hardware reaching TRL 7-8.

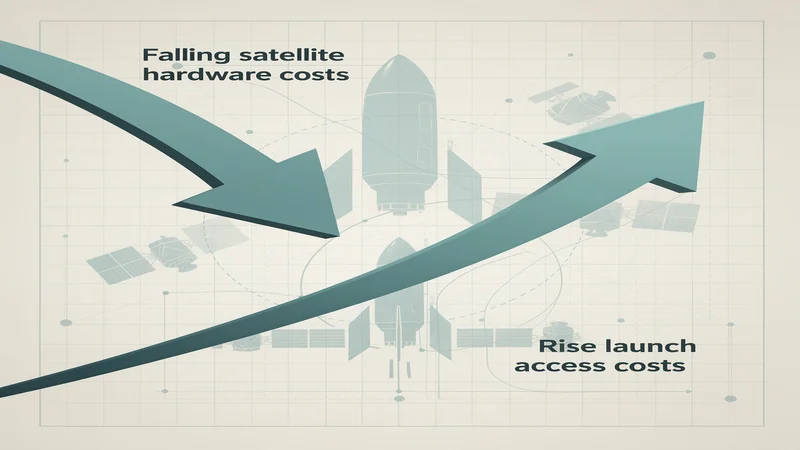

- SmallSat unit costs and launch costs are diverging: demonstrated mission costs range from $2-5M while SpaceX rideshare pricing rises at $500/kg per year against a monopoly baseline of $6,000-$6,500/kg.

- No developing nation has achieved sovereign, operationally exploited space-derived climate or disaster resilience capability via SmallSats; the financing and governance domain remains at TRL 2-3.

- The 2026-2028 window represents the cost-performance sweet spot for program entry; delay yields worse terms across launch costs, regulatory burden, and orbital congestion.

- Data-as-a-service from commercial constellations is already a competing S-curve in its growth phase, shifting the strategic rationale for national SmallSat programs from operational utility toward sovereignty and industrial development.

Executive Summary

This assessment examines whether SmallSat technology can enable developing nations to achieve operationally useful space capabilities for climate monitoring and disaster resilience without replicating the institutional infrastructure of legacy space powers. The analysis reveals a fundamental temporal mismatch: the hardware cost window is favorable now, while the institutional capacity required to exploit that hardware demands a decade or more to build. The central strategic insight is that SmallSats have opened a real but fragile access window, and the nations best positioned to benefit are those that have already begun – not those still deliberating.

The Technology Landscape

The SmallSat revolution has delivered on its most visible promise: a satellite that once cost hundreds of millions of dollars can now be built and launched for under five million. But this headline obscures a deeper question about whether affordable hardware translates into usable capability – and whether the window of affordability itself is sustainable.

Context and Focal Question

Developing nations face mounting pressure from climate change and natural disasters, and space-based Earth observation offers a powerful tool for monitoring, early warning, and resilience planning. SmallSats – spacecraft under 180 kg , with the smallest classes often built from commercial off-the-shelf components – have been championed as the vehicle for democratizing this capability. Botswana’s BOTSAT-1 reached orbit for $2.19 million . Mexico’s MXAO-1 flew for under five million . International programs like KiboCUBE and UNOOSA-Exolaunch provide subsidized launch slots for nations from Bolivia to Nepal.

The focal question is whether these entry points represent genuine democratization or merely the illusion of access – and if the window for meaningful sovereign space capability is narrowing faster than most nations can walk through it.

The Driving Trends

Six trends define the SmallSat landscape for developing nations, and their interactions matter more than any single trend in isolation.

First, COTS platform commoditization has driven satellite hardware costs to near their floor. The S-curve for SmallSat unit costs is in late growth approaching maturity, with demonstrated complete mission costs reduced to $50,000-$5,000,000 depending on complexity and available resources .

Further reductions require architectural leaps – software-defined payloads, printed structures – that remain three to five years from flight readiness.

Second, and working against the first, launch access costs are rising rather than falling . SpaceX’s rideshare program, which catalyzed the SmallSat market from 2021, now operates as a near-monopoly priced at $7,000 per kilogram with explicit annual increases. This is not a technology ceiling but a market-structure phenomenon: the gap between marginal launch cost and market price represents economic rent that only competition can erode.

Third, regulatory compliance costs are accumulating. The FCC’s five-year deorbit rule requires propulsion systems for CubeSats above approximately 600 km , adding significant cost and complexity at the lowest tier. Spectrum allocation requirements layer additional barriers. The net cost trajectory for a regulation-compliant mission is less favorable than raw hardware prices suggest.

Fourth, the operational capability gap persists. Chile’s FASat-Delta remained non-operational 300 days after launch . Chile’s civilians could not access FASat-Charlie data during wildfire emergencies despite the satellite being available. The historical SmallSat failure rate of approximately 40 percent – a figure spanning two decades of all satellite classes, with current rates likely lower – driven primarily by software and systems integration rather than hardware, imposes disproportionate risk on nations with no budget margin for mission loss.

Fifth, data-as-a-service from commercial operators – Planet, Spire, ICEYE – is already a competing adoption curve in its growth phase, offering developing nations Earth observation data without the cost and complexity of satellite ownership.

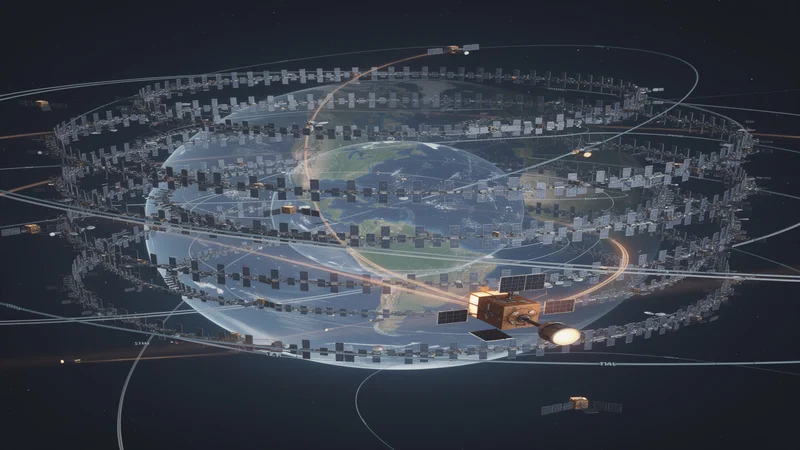

Sixth, megaconstellation expansion is consuming orbital and spectrum resources at an accelerating pace. China’s 200,000-plus ITU satellite filings and SpaceX’s 10,000-plus active satellites suggest that the orbital environment may become structurally inhospitable for small national programs within a decade.

“Horizon” Summary

| Horizon | Focus | Assessment | Key Insight |

|---|---|---|---|

| H1 Maintain & Defend (0-2y) | COTS procurement, rideshare access, international programs, university pipelines | Under Pressure – access is real but terms are deteriorating | The cost of satellite hardware is falling but the cost of useful operations is not |

| H2 Build & Scale (2-5y) | Indigenous manufacturing, national constellations, shared ground infrastructure | Mixed – South Africa proves the pathway but Chile and ALCE show the barriers | The transition from buyer to space-capable nation demands institutional depth most developing nations lack |

| H3 Explore & Transform (5+y) | Pooled-sovereignty cooperatives, AI-driven autonomy, climate finance | Exposed – governance barriers stall cooperation; megaconstellation saturation may close the window | The question is not whether SmallSats can democratize access but whether the window stays open long enough |

The Three Horizons

The choices developing nations make in the next two to three years will determine which futures remain accessible. Each horizon presents a distinct strategic posture, but the transitions between them are where programs succeed or stall.

Horizon 1: Access Is Real but Fragile

The near-term SmallSat landscape offers developing nations genuinely unprecedented entry points. Missions at the $2-5 million total cost level are demonstrated facts, not projections, and eight rounds of the KiboCUBE program since 2015 have provided launch opportunities to nations that could never have accessed orbit otherwise. SpaceX’s Transporter-16 carried 119 payloads in March 2026 , with over 1,000 cumulative rideshare deployments to date .

But a technology readiness assessment reveals that this access is far shallower than it appears. Satellite bus and payload hardware sits comfortably at TRL 7-8 – flight-proven and reliable. The system as a whole, however, is gated by the weakest link. Ground segment capability in developing-nation contexts rates at TRL 5-6, with cloud-based services like AWS Ground Station and open networks like SatNOGS available but largely unadopted. Mission operations and data exploitation – the ability to turn orbital assets into actionable disaster warnings or climate data – sits at TRL 3-5. The overall system readiness is therefore TRL 3-5, regardless of how mature the satellite hardware is.

This gap has concrete consequences. Botswana’s BIUST built BOTSAT-1 with approximately 80 volunteers who delivered a flight-qualified satellite, but volunteer-dependent programs struggle with continuity and quality assurance. Egypt has established assembly, integration, and testing capability , representing a genuine institutional achievement. For most developing nations, though, the gap between launching a satellite and operating a space program remains vast. Three structural pressures are intensifying simultaneously: rideshare monopoly pricing erodes cost advantages, the operations gap consumes budgets that should be building capability, and each failed mission carries disproportionate consequences where there is no margin for redundancy.

The critical question for H1 is not whether access exists, but whether programs can convert one-off satellite procurements into sustained operational capability before the terms of access deteriorate further.

Horizon 2: The Narrow Path from Buyer to Builder

Six South African companies supplied 116 products to SpaceX’s Transporter-14 , with Dragonfly Aerospace supplying Earth observation payloads globally. This represents a genuine shift from end-user to supply-chain participant – but it required decades of sustained industrial policy, not a SmallSat-era shortcut.

The path South Africa blazed is narrow and poorly mapped for followers. A convergence analysis reveals that operational space capability requires four domains to mature simultaneously: hardware technology, launch access, institutional and human capital, and financing and governance architecture. No single domain is sufficient. The weakest – financing and governance, at TRL 2-3 – determines the pace of the whole system. The Latin American and Caribbean Space Agency (ALCE), launched in 2021 with 21 signatories, has stalled before becoming operational. Brazil, the region’s largest space actor, is absent. The most promising governance pathway has failed its first test.

Several H2 opportunities are maturing. National constellation programs for climate and disaster monitoring are in early design, with an academic study proposing a 12-satellite constellation for India at $0.75 million per unit . Shared ground infrastructure is reducing what has been the most underestimated cost barrier. CubeSat propulsion systems are advancing toward the regulatory compliance that will become mandatory.

But every opportunity faces structural headwinds. The flight-proven paradox blocks technology adoption: new systems cannot gain heritage without flying, but buyers demand heritage before purchase. Traditional catch-up industrial policy – the protected-market strategy that worked for semiconductors and automobiles – does not transfer to space, where global regulatory and competitive standards apply from inception. South Korea’s $290 million space cluster strategy is discovering this constraint in real time.

The critical question for H2 is whether developing nations can build institutional depth fast enough to exploit the current hardware cost window – or whether the 7-12 year timeline that convergence analysis suggests for mid-tier nations will overshoot the period of favorable access.

Horizon 3: Closing Windows and Alternative Paths

The long-term transformative possibilities for developing-nation space access are real but contingent on governance innovations that have no demonstrated precedent. Pooled-sovereignty constellation cooperatives – shared orbital assets reducing per-nation costs by an order of magnitude – represent the most impactful possibility, but ALCE’s stall suggests governance barriers exceed technical ones. AI-driven autonomous satellite operations could leapfrog the persistent ground segment gap, though on-board machine learning inference has not yet been miniaturized for CubeSat power and compute budgets. Climate finance instruments, following the model of Italy’s IRIDE constellation funded through the EU’s National Recovery and Resilience Plan , could unlock multilateral development bank capital for space assets – but no developing-nation application exists.

The most consequential H3 dynamic is not a missed opportunity but a closing door. Megaconstellation operators are accumulating orbital slots and spectrum allocations at a pace that could structurally foreclose options for small national programs. Late entrants may face not merely higher costs but genuinely closed access. Meanwhile, the data-as-a-service model offers an alternative convergence pathway that bypasses satellite ownership entirely, delivering Earth observation data by converging only two domains – commercial supply and institutional data exploitation – rather than the full four-domain convergence that sovereign capability requires.

The critical question for H3 is whether developing nations should pursue sovereign SmallSat capability as a long-term industrial development goal while meeting immediate disaster resilience needs through commercial data procurement – or whether the window for sovereign access will close before that bifurcated strategy can bear fruit.

Transition Dynamics

The H1-to-H2 transition is already underway in a handful of nations. South Africa’s component manufacturing and Egypt’s assembly and testing capability represent genuine H2 achievements built on decades of investment. For most developing nations, however, the transition from one-off CubeSat missions to sustained capability remains blocked by institutional gaps more than technical ones. The most achievable near-term transition is launch access diversification: as Indian commercial rideshare scales and Chinese commercial launch matures, the SpaceX monopoly will face its first real competitive pressure within two to three years.

The H2-to-H3 transitions are largely contingent on governance breakthroughs. Pooled sovereignty requires successful regional frameworks that have not yet materialized. Climate finance for space assets requires multilateral development bank architecture that does not yet exist. The window for these transitions is narrowing as megaconstellation operators accumulate resources, creating urgency that the current pace of institutional development cannot match.

The Outlook

The horizon analysis reveals a landscape where timing is the decisive variable. The technology is ready, the access points exist, and the need is urgent. What is missing is the institutional and financial architecture to connect these elements – and the clock is running against the nations that need it most.

What Each Horizon Demands

Now (H1). Developing nations should prioritize ground segment and data exploitation investment over satellite hardware. Every dollar spent on ground stations, data processing pipelines, and end-user integration yields higher returns than incremental satellite capability. Launch access must be diversified immediately – engaging ISRO commercial rideshare, Chinese providers, and launch brokers to reduce exposure to SpaceX monopoly pricing. For immediate disaster resilience needs, commercial Earth observation data from Planet, Spire, and ICEYE should be procured now rather than waiting for national satellites to become operational. Building the institutional capacity to exploit third-party data is itself preparation for exploiting future sovereign satellite data.

Build (H2). Investment should target systems integration capability, not just satellite engineering. The gap between launching a satellite and operating a space program is institutional: it requires multi-year funded positions for mission operations engineers, ground segment specialists, and data scientists – not project-based contracts that dissolve when a mission ends. Regional cooperation should be pursued through bilateral and trilateral arrangements rather than waiting for continental governance to crystallize. Climate finance instruments that include space assets should be actively advocated within multilateral development bank frameworks, following the IRIDE precedent.

Explore (H3). Megaconstellation orbital and spectrum saturation must be monitored as a potential foreclosure event for small national programs. AI-driven autonomous satellite operations – the single most transformative technology for eliminating the ground segment dependency that constrains developing nations – deserve dedicated tracking and early experimentation. The bifurcated strategy of procuring data for immediate needs while building sovereign capability over a longer timeline should be explicitly adopted rather than allowed to emerge by default.

Limitations

This assessment spans time horizons where discontinuous disruption – policy reversals, launch failures, orbital debris events – could reshape the landscape overnight. The approximately 40 percent historical SmallSat failure rate spans two decades and all satellite classes; current rates for COTS platforms are likely lower but are not publicly documented at sufficient granularity. The analysis assumes international propagation of regulatory trends like the FCC deorbit rule; exemptions or non-compliance would lower cost burdens but increase debris externalities. Developing nations are not a monolithic category, and while this analysis distinguishes frontrunners from mid-tier and late-entry nations, granularity is constrained by the absence of any fully converged reference case. Military and dual-use motivations, which may dominate civilian rationales in some national contexts, are excluded. The three-horizons framework imposes structured temporality on dynamics that may not respect neat boundaries.

Primary Sources & Research

JAXA (2024). KiboCUBE Program: 8th Round Selection Results. JAXA Global. https://global.jaxa.jp/press/2024/07/20240730-2_e.html

ESA (2026). Eight More Satellites Added to IRIDE Space Programme. European Space Agency. https://www.esa.int/Applications/Observing_the_Earth/IRIDE/Eight_more_satellites_added_to_IRIDE_space_programme

NASA (2024). State-of-the-Art Small Spacecraft Technology Report. NASA Small Spacecraft Virtual Institute. https://www.nasa.gov/smallsat-institute/sst-soa/

Aerospace Corporation (n.d.). FCC 5-Year Deorbit Rule: Implications for SmallSat Operators. Aerospace Corporation. https://aerospace.org/node/50785/printable/print

Aerospace Corporation (n.d.). The Flight-Proven Paradox in SmallSat Technology Adoption. Aerospace Corporation. https://aerospace.org/node/51858/printable/print

CSIS / Laura Delgado Lopez (2024). Orbital Dynamics: Domestic and Foreign Policy Forces Shaping Latin American Engagement. Center for Strategic and International Studies. https://csis.org/analysis/orbital-dynamics-domestic-and-foreign-policy-forces-shaping-latin-american-engagement

East Asia Forum / Monique Taylor (2026). Starlink, China and the Governance of Low Earth Orbit. East Asia Forum. https://eastasiaforum.org/2026/02/19/starlink-china-and-the-governance-of-low-earth-orbit/

Carnegie Endowment / Draudt-Vejares and Kim (2025). South Korea’s Industrial Policy for the New Space Economy. Carnegie Endowment for International Peace. https://carnegieendowment.org/research/2025/10/south-koreas-industrial-policy-for-the-new-space-economy?lang=en

Space in Africa (2025). Egypt Launches SPNEX Satellite, Advances Domestic Space Manufacturing. Space in Africa. https://spaceinafrica.com/2025/12/14/egypt-launches-spnex-satellite-advances-domestic-space-manufacturing/

Space in Africa (2025). South African Space Companies Supply Over 100 Products in Latest SpaceX Transporter-14 Launch. Space in Africa. https://spaceinafrica.com/2025/07/03/south-african-space-companies-supply-over-100-products-in-latest-spacex-transporter-14-launch/

Sah, Srivastava, and Das (2021). Low-Cost Constellation Design for Infrastructure Monitoring over India. arXiv. http://arxiv.org/abs/2107.09253v1

Spence et al. (2022). Achievements and Lessons Learned from Successful Small Satellite Missions for Space Weather-Oriented Research. arXiv. https://arxiv.org/abs/2206.02968

Caspi et al. (2022). Small Satellite Mission Concepts for Space Weather Research and as Pathfinders for Operations. arXiv. https://arxiv.org/abs/2201.07426