The Third Way Under Stress: Can IRIS² Be a Sovereign Utility Instead of a Starlink Rival?

Key Findings

- Scale asymmetry is structural: IRIS²’s ~290 satellites (264 LEO + 18 MEO) face Starlink’s ~7,000–9,000 deployed (target 42,000), Kuiper’s ~3,200, and China’s Guowang/Qianfan at 13,000–15,000 planned.

- Capacity-per-euro is the binding constraint: ~3.3 Tbps total (~2 Tbps LEO), roughly two Starlink V3 satellites’ worth , against Telesat Lightspeed’s ~10 Tbps from fewer than 200 satellites.

- Cost roughly doubled from ~€6bn to €10.6bn during ideation, with in-service slipping 2024 → 2026 → 2028 → 2030 → potentially 2031.

- Funding is thin: only €2.4bn of the ~€6.5bn public envelope is firmly committed , with the balance dependent on a post-2027 budget not yet voted.

- Four of Porter’s five forces are adverse; the sole favourable force (entry barriers) also entrenches the high-cost suppliers driving the overruns.

- Realised LEO demand is government-led: Eutelsat’s OneWeb revenue rose 84% to €187M with a €1bn ten-year French military contract , while commercial broadband demand in fibre-rich Europe is questioned by McKinsey and ESPI.

Executive Summary

This analysis examines whether IRIS²’s hybrid “Third Way” model, blending institutional security with commercial ambition, is a viable competitive position against Starlink and the megaconstellation field. The structural picture is stark: as a commercial broadband contender the industry is unattractive and the entrant is outgunned on scale, cost, and timing, yet the same programme reads as defensible when scoped as a sovereign-infrastructure utility rather than a Starlink rival. The strategic insight is that IRIS²’s advantages and vulnerabilities do not net out to “average”; they bifurcate cleanly by segment, which makes the framing decision, not the technology, the decisive variable.

The Industry

Few industries punish a late institutional entrant as thoroughly as satellite broadband, where the incumbent is already operational, cheaper per bit, and scaling toward forty thousand satellites while the challenger has yet to launch one. The defining tension is that the same market looks attractive when defined by European sovereignty and unattractive when defined by global price and performance.

IRIS² enters a market whose competitive physics reward volume and vertical integration, carrying a deliberately small fleet and a sovereignty mandate that volume economics cannot price.

Context and Industry Definition

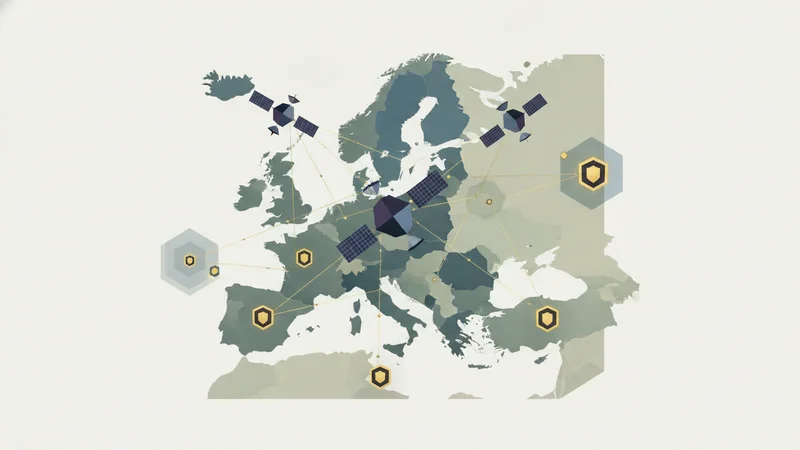

The relevant industry here is secure and commercial satellite broadband in and for the European market, spanning two very different demand tiers: an institutional government and defence tier, and a contested commercial broadband tier. The boundary is deliberately drawn around the European market as a protected demand space rather than the global broadband market, because IRIS²’s entire strategic logic rests on sovereignty and regulatory levers that have force only inside EU jurisdiction. That choice is itself the central analytical move. A market bounded by sovereignty looks defensible; the same market bounded by global competition looks lost before launch.

The programme’s own architecture encodes the split. Services tier into “Hard Gov” for government-authorised users, “Light Gov” plus commercial, and a next-generation Low-LEO layer including direct-to-device , sitting under a twelve-year concession signed in December 2024 between the European Commission and the SpaceRISE consortium of SES, Eutelsat, and Hispasat, with ESA as technical overseer. Only the commercial tier competes head-to-head with Starlink; the government tiers rest on EU-anchored demand. The stakeholders that matter most are therefore not symmetric rivals but a single anchor buyer, a reluctant channel of telco partners, and a supplier base the programme cannot easily discipline.

The Competitive Landscape

The rivalry IRIS² faces is not a contest among peers but an asymmetric confrontation between a sub-scale institutional latecomer and hyperscale commercial incumbents. Starlink defines the basis of competition through vertical integration and low unit cost; Amazon Kuiper validates that scale plus ecosystem bundling is the dominant model; the Chinese state constellations add state-backed volume in non-EU markets. Against this field IRIS² is the only entity competing on sovereignty rather than scale, a stance that both differentiates it and exiles it from the volume economics the others enjoy. The capacity-per-euro gap is the spine of the problem. A full constellation expected to yield roughly 3.3 Tbps, the LEO portion equivalent to about two Starlink V3 satellites, costs a multiple of what incumbents pay for far more throughput, and Telesat Lightspeed’s ~10 Tbps from fewer than 200 satellites shows the gap is not intrinsic to small fleets but specific to this one. That capacity figure is a single medium-reliability analyst estimate rather than an official specification, and is weighted accordingly, but it is physically consistent with the known area-capacity ceilings of LEO systems.

If rivalry is the external pressure, substitution is the more acute one, because Starlink is not a future threat but a present product. Academic consensus frames satellite as a complement to terrestrial networks rather than a standalone broadband substitute in dense, fibre-rich Europe, which narrows the commercial opening further. The sharpest dynamic is a timing trap: with IRIS² services not arriving before 2030, every interim Starlink contract a member state signs is demand the programme may never recover. GOVSATCOM pooling of existing Member-State capacity bridges near-term government needs and reduces urgency on the one tier where IRIS² is strong, which paradoxically removes pressure to commit early.

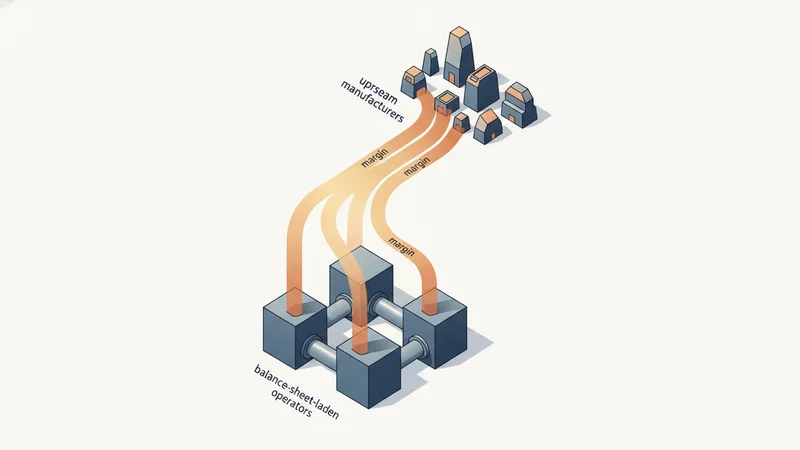

These pressures are mirrored inside the value chain by supplier power that is structural rather than negotiated. Sole-source authorisations to proceed went to Thales Alenia Space and Airbus, bypassing competitive bidding, while ESA’s geographic-return principle entrenches a fragmented, higher-cost supplier base. The reconciled reading of the apparent contradiction here is itself revealing: the primes declined to take equity stakes, leaving SES, Eutelsat, and Hispasat to “hold the bag,” yet they still collect the manufacturing awards. They will build IRIS² but would not underwrite it, extracting contractor margin while declining programme downside. Launch compounds the squeeze, since Ariane 6 runs roughly ten flights a year against a thirty-launch backlog that already includes eighteen for Kuiper, so European launch sovereignty competes with a US commercial customer for scarce slots.

Buyer power completes the adverse set, and does so in a way that the institutional anchor was supposed to prevent. On paper the European Commission de-risks demand as the single anchor customer, but the operative buyers, the consortium’s own telco channel partners Orange and Deutsche Telekom, refuse captive commitment and will buy only if IRIS² is price and performance competitive with Starlink and Kuiper . Eutelsat’s own chief executive conceded the programme “must compete on price and performance to win customers.” The exit clauses sharpen the asymmetry: a material overrun, slip, or underperformance gives any operator the right to walk, so the public sector is simultaneously the anchor buyer and the residual risk-bearer. The one force that runs in IRIS²’s favour, the near-impossibility of new entry, is double-edged. The capital, spectrum, and launch barriers that shield IRIS² are the very barriers that protect its high-cost incumbent suppliers and blunt the SME cost innovation it would need to close the gap.

Seen through the lens of disruption, this configuration is not a balanced rivalry at all but the signature of an incumbent meeting a disruptor with the wrong reflex. Starlink is a genuine new-market disruptor that changed the basis of competition from heritage and reliability to scale, cost, and iteration, and has since moved upmarket into institutional demand. IRIS²’s consortium members are precisely the legacy operators that disruption displaced. The textbook failure mode follows: answering a cost-disruptor by building something more sophisticated and more expensive, a multi-band, multi-orbit, hard- and light-gov system whose “too many competing requirements” are the industry-language version of over-serving. The cost doubling to €10.6bn and the repeated slips are exactly what the theory predicts when an incumbent escalates sophistication instead of restructuring economics.

Five Forces Summary

| Force | Intensity | Key Driver | Trend |

|---|---|---|---|

| Competitive Rivalry | High | Scale and capacity-per-euro asymmetry vs Starlink/Kuiper | Increasing |

| Threat of New Entrants | Low | Prohibitive capital, spectrum, launch barriers | Stable |

| Threat of Substitutes | High | Operational Starlink, terrestrial fibre, timing trap | Increasing |

| Supplier Power | High | Sole-source primes, juste retour, launch scarcity | Stable |

| Buyer Power | High | Conditional channel demand, part-committed anchor, exit clauses | Increasing |

Overall Industry Attractiveness: Unattractive

The Value Dynamics

External forces explain why the market is hard to win; the value chain explains who actually keeps the money, and the answer is uncomfortable for the entity that bears the most risk. Value in this programme is migrating away from the operators who carry the capital and toward the suppliers who carry none.

Meanwhile the commercial value that was supposed to justify the build leaks out of the chain entirely toward Starlink.

Where Value Lives

The strategically significant activities in IRIS²’s chain are operations and service, and both concentrate value in the sovereign tier rather than the commercial one. Operations is where engineered sovereignty actually lives: laser inter-satellite links routing traffic to only five European ground points-of-presence, deliberately avoiding uncontrolled terrestrial infrastructure, backed by spectrum-priority rights inherited from OneWeb and O3b mPOWER that rank ahead of Starlink in LEO . Service is where differentiation is genuinely strong, but only in the government tier, through sovereign quantum-secure connectivity built on the EuroQCI infrastructure backed by all twenty-seven Member States . The technology-development activity that should compound these advantages is instead constrained, with 7nm chips deferred and an agility gap that academic and industry sources both flag, where commercial operators iterate faster than institutional consortia.

The pattern of value capture is where the structure turns against IRIS². The primes capture high margin at low risk, building without underwriting; the operators carry the capital, the debt, and the exit-option overhang while capturing thin operating margin; and the commercial-broadband segment captures little because the value migrates to the substitute. Two chokepoints govern the whole chain, launch cadence and sole-source prime manufacturing, and both sit with suppliers IRIS² cannot discipline, which is exactly why they translate into schedule slip and cost growth rather than mere friction. The business-model reading sharpens this into a coherence verdict: the programme tries to carry two incompatible value propositions on one inflated cost base. The sovereign proposition is coherent, with differentiated value, defensible demand, and regulatory protection. The commercial proposition is not, with undifferentiated value, demand that McKinsey and ESPI doubt, and a channel that will not commit.

The financeability picture confirms the diagnosis. Operator balance sheets are stretched, Eutelsat carrying €2.7bn of debt and SES €4.57bn at end-2024, recapitalised through French and UK state participation rather than private markets, so the “sovereign” model is funded through sovereign guarantees. Private investors at SmallSat Europe judged the ~€4.1bn private share unraisable , with one principal calling IRIS² “dead in the water.” Against that, the one assumption that holds is sovereign demand: Eutelsat’s OneWeb revenue up 84% to €187M and a €1bn ten-year French military deal show the viable near-term market is institutional, not consumer. The nearest viable analogue is therefore not Starlink’s self-funding commercial model but a sovereign utility on the Galileo and Copernicus pattern , where success is measured by strategic-autonomy delivery rather than commercial return.

Competitive Position

This is where the two lenses converge, and the convergence is unusually clean. IRIS²’s competitive exposure and its value-chain weakness coincide in the commercial tier, where it is exposed to rivalry and substitutes, weak in sales, and leaking value to Starlink. Its protection and its strength coincide in the government tier, where it is entry-protected, substitute-immune, strong in service, and able to defend its margin. The advantages, engineered topology, spectrum priority, quantum security, and regulatory protection, all cluster on the non-market side; the vulnerabilities, cost base, launch dependency, conditional demand, and the funding gap, all cluster on the commercial side.

The analytical payoff is that IRIS² is mis-scoped if treated as a broadband competitor and correctly scoped if treated as a sovereign-infrastructure utility. The non-market levers Europe is deploying are real but limited in what they can do. Reserving roughly two-thirds of future 2 GHz mobile-satellite spectrum for European operators , and the forthcoming EU Space Law imposing cybersecurity and resilience requirements on any EU-market operator, can make a rival “structurally inferior” inside Europe and buy protected share. They cannot close the capacity gap or manufacture commercial demand, and they are politically reversible, which is the central strategic tension: the EU is erecting protections for IRIS² at the same moment its own consortium telcos insist they will buy only on competitive merit.

The Outlook

The structure does not demand that IRIS² win the broadband market; it demands that IRIS² stop trying to. Everything that is strong about the programme lives in one segment, everything that is failing lives in the other.

The strategic task is to recognise the difference and act on it before the timing trap and the funding cliff foreclose the choice.

Strategic Implications

On industry positioning, IRIS² should present itself explicitly as a sovereign-infrastructure utility rather than a Starlink competitor, competing on the sovereignty axis (jurisdiction-independent topology, quantum security, regulatory trust) where it is structurally strong and conceding the commercial-broadband axis where it is structurally exposed. The civil dimension supports this, with member states already running interim rural and school connectivity budgets that a sovereign backbone can anchor by 2030.

On value chain focus, investment should concentrate in the service and operations activities that embed sovereignty: the laser ISL topology, the five-PoP architecture, and EuroQCI integration. The supplier-power chokepoint is the internal source of the overrun pattern, so relaxing geographic return where feasible is the highest-leverage cost intervention available, and attention spent on undifferentiated commercial sales is attention wasted. The risk that military requirements may not be fully integrated deserves early correction, since a system that satisfies neither commercial economics nor military utility would fail on both axes at once.

On what to monitor, the leading indicators are concrete and near-term. First, the post-2027 funding votes and the €2.4bn-to-€6.5bn commitment gap , the single clearest signal of political will. Second, operator exit-clause triggers and Eutelsat and SES solvency, which determine whether the private partners stay. Third, member-state Starlink contracting, which activates the timing trap. Fourth, the trajectory of spectrum reservation and the EU Space Law, treated as time-buying rather than gap-closing. Fifth, design-freeze and descope events as the leading indicators of further overrun.

Limitations

The decisive analytical choice is the industry boundary. Bounding the market as European protected demand rather than global broadband is what makes the government tier look defensible; a global-market definition would render IRIS² straightforwardly uncompetitive, and the chosen boundary must not be mistaken for a claim of global competitiveness. Several load-bearing data points are single-source and weighted down accordingly: the ~3.3 Tbps capacity figure (a medium-reliability analyst estimate, not an official spec), the operator exit clauses and >10% IRR terms, the €2.4bn firm-commitment figure, and the anti-Starlink-lobbying claim. The structural and business-model frameworks are point-in-time snapshots of a programme still pre-launch, so the assessment will shift at every funding and descope event, and disruption outcomes are projected as ranges rather than points. The analysis assumes sovereign and defence demand is durable and that political funding continues at least at sovereign-utility scale; if strategic-autonomy momentum reverses or member states default to Starlink in the gap, even the conditional-viability reading fails. Macro-environmental, full governance, and security-threat analyses were left to adjacent specialist lenses, and one cited source carries disclosed Amazon and SpaceX funding whose pro-US-commercial framing is weighted accordingly.

Primary Sources & Research

European Space Agency (2024). ESA programme related to EU Secure Connectivity and IRIS². ESA Connectivity & Secure Communications. https://connectivity.esa.int/esa-programme-related-to-eu-secure-connectivity-and-iris%C2%B2

European Space Agency (2025). ESA invites new proposals for the EU Secure Connectivity Programme. ESA Connectivity & Secure Communications. https://connectivity.esa.int/news/esa-invites-new-proposals-eu-secure-connectivity-programme

European Space Agency (2024). ESA confirms the kickstart of IRIS² with the European Commission and SpaceRISE. ESA Connectivity & Secure Communications. https://connectivity.esa.int/archives/news/esa-confirms-kickstart-iris%C2%B2-european-commission-and-spacerise

European Space Agency (2026). ESA and Spain sign agreement to advance Europe’s secure connectivity future. ESA Connectivity & Secure Communications. https://connectivity.esa.int/archives/news/esa-and-spain-sign-agreement-to-advance-europes-secure-connectivity-future

European Space Agency (2025). Funding opportunity: consolidation phase for IRIS² Low-LEO pre-operational and de-risk activities. ESA Connectivity & Secure Communications. https://connectivity.esa.int/archives/opportunities/funding-opportunity-consolidation-phase-for-iris2-low-leo-pre-operational-and-de-risk-activities

European Space Agency (2023). ESA to support the development of EU’s secure communication satellites system. ESA Corporate News. https://www.esa.int/About_Us/Corporate_news/ESA_to_support_the_development_of_EU_s_secure_communication_satellites_system

European Space Agency (2023). ESA works with EU on secure connectivity. ESA Corporate News. https://www.esa.int/About_Us/Corporate_news/ESA_works_with_EU_on_secure_connectivity

European Space Agency (2024). Europe chooses resilient and secure space-enabled connectivity with €2.1 billion investment. ESA Applications. https://www.esa.int/Applications/Connectivity_and_Secure_Communications/Europe_chooses_resilient_and_secure_space-enabled_connectivity_with_2.1_billion_investment

European Space Agency / European Commission (2025). ESA and the European Commission sign EuroQCI implementation agreement. ESA Multimedia. https://www.esa.int/ESA_Multimedia/Images/2025/01/ESA_and_the_European_Commission_sign_EuroQCI_implementation_agreement

European Commission (DG DEFIS) (2024). Commission takes next step to deploy IRIS² secure satellite system. European Commission, Defence Industry and Space. https://defence-industry-space.ec.europa.eu/commission-takes-next-step-deploy-iris2-secure-satellite-system-2024-12-16_en

European Space Policy Institute (2025). IRIS² growing up: from strategic roots to commercial power play. ESPI Briefs. https://www.espi.eu/briefs/iris%C2%B2-growing-up-from-strategic-roots-to-commercial-power-play/

European Space Policy Institute (2021). About a new European multi-orbit connectivity system. ESPI Briefs. https://www.espi.eu/briefs/about-a-new-european-multi-orbit-connectivity-system/

European Space Policy Institute (2025). ESPI Report 94: European space defence. ESPI. https://www.espi.eu/wp-content/uploads/2025/03/ESPI-Report-94.pdf

Center for Strategic and International Studies (2025). Strategic ambition vs structural dependency: why Europe can’t stand alone in space. CSIS Europe Corner. https://www.csis.org/blogs/europe-corner/strategic-ambition-vs-structural-dependency-why-europe-cant-stand-alone-space

CSIS Aerospace Security Project (2023). Low Orbit, High Stakes. CSIS. https://aerospace.csis.org/wp-content/uploads/2023/02/221214_Young_LowOrbit_HighStakes-min.pdf

Center for Space Policy and Strategy (Aerospace) (2024). The New EU Space Law. Aerospace Corporation / CSPS. https://csps.aerospace.org/sites/default/files/2024-11/05a_NewEUSpaceLaw_Gleason_20241104.pdf

Stimson Center (2023). A European perspective on space in an era of strategic competition and transformation. Stimson. https://www.stimson.org/2023/a-european-perspective-on-space-in-an-era-of-strategic-competition-and-transformation/

Observer Research Foundation (2025). Space geopolitics: Europe’s call for autonomy. ORF Expert Speak. https://www.orfonline.org/expert-speak/space-geopolitics-europe-s-call-for-autonomy

Observer Research Foundation (2025). Critical commercial infrastructure in warfare: the new face of grey zone. ORF Expert Speak. https://www.orfonline.org/english/expert-speak/critical-commercial-infrastructure-in-warfare-the-new-face-of-grey-zone

Sedin, J., Feltrin, L. & Lin, X. (2020). Throughput and Capacity Evaluation of 5G New Radio Non-Terrestrial Networks with LEO Satellites. arXiv. http://arxiv.org/abs/2012.02136v1

Sun et al. (2025). Visibility-aware Satellite Selection and Resource Allocation in Multi-Orbit LEO Networks. arXiv. http://arxiv.org/abs/2511.12678v1